Atal Pension Yojana Benefits : How to apply, Online Registration

Atal Pension Yojana

The Atal Pension Yojana is a government program that encourages individuals to save money for future usage. Therefore, those who desire to save a little sum for a fixed pension might do so under this Scheme after they retire.

Further brief of this Scheme reveals that it is also known as Swavalamban Yojana, which means “Self-Support.” That’s why it’s also known as a Self-Support Scheme. It is a government-sponsored pension program in India largely aimed at the unorganized sector. However, people working in the private sector who are neither taxpayers nor members of any other social security plan can also benefit from it. Furthermore, all qualified family members can enroll in APS in their names to get increased pension plan benefits for their families.

Basic Details

| Scheme | Atal Pension Yojana |

| Launched By | Prime Minister Narendra Modi |

| Launched On | 9 May 2015 in Kolkata. |

| Eligibility Age | 18- 40 are eligible for pension |

| Targeted Benifieries: | Unorganized sector |

| Pensions Amount | 1000 – Rs.5000 |

| Application | Offline.( Contact near bank branch)/Online |

| The minimum contribution duration | 20 years. |

| Application Download From | PFRDA’s website. |

| Online link | https://www.npscra.nsdl.co.in/scheme-details.php |

Eligibility Criteria

- To qualify, the applicant must be between 18 and 40. This means that the minimum contribution period is 20 years, after which the subscriber can take a monthly pension.

- To enable additional payments, the subscriber must have a KYC-compliant active bank account and maintain a minimum level in the bank account sufficient to permit monthly debit of their payment.

- Should not be a beneficiary of any other similar social security plan.

- The aspirant should not be a participant in a company-sponsored scheme or any other program that promises a monthly pension after retirement.

- Should guarantee continuous monthly contributions until retirement age is reached. Any failure to make monthly payments on time may result in account cancellation.

- Active Swavalamban Yojana NPS Lite participants will be transferred to the Atal Pension Yojana Scheme.

Need for APY

- A pension is a monthly income that people get after they are no longer working.

- Income earning potential declines with aging.

- Earning members in nuclear families are increasingly migrating.

- Cost of living increases.

- Prolonged life expectancy.

- A monthly income guarantee provides a decent life in old age.

Click Here for Kisan Nidhi Yojana

APY Features

Role in contributing to Boosting Feature

Active Swavalamban Yojana NPS Lite participants will be transferred to the Atal Pension Yojana. As previously stated, you are entitled to earn a pension from the Atal Pension Yojana after you reach the age of 60. The amount of your pension is determined by your contribution to this program. Varied contributions result in different pension amounts. As a result, you may elect to make bigger payments in order to receive a larger pension later. The government of India allows increasing and decreasing facilities for the amount of contribution to change the amount of corpus. This support is available once a year.

Automatic Debit

The APY is one of India’s most well-known and popular pension systems. As a beneficiary, you may link your bank account to your APY account and have your payments deducted straight from your account. The linked account should have a sufficient balance to prevent automatic debit from failing, which might result in a penalty.

Guaranteed Pension

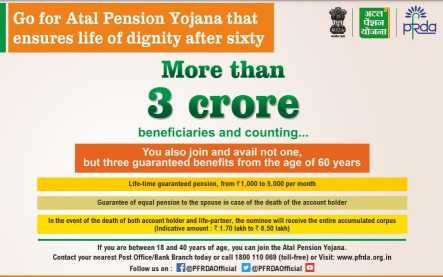

As an Atal Pension Yojana recipient, you are entitled to a monthly pension of Rs. 1000, Rs. 2000, Rs. 3000, Rs. 4000, or Rs. 5000 based on your monthly payment.

Withdrawal Policies

But if you’re a beneficiary of the Atal Pension Yojana (APY), you can annuitize the whole corpus amount. After closing this program with your bank, you will get a monthly pension. However, you can leave the plan before the age of 60 only if you have a serious disease or death.

Age Restrictions

Undergraduate students can enroll in the Atal Pension Yojana to build a corpus for their retirement. The maximum age for this program is set at 40 years. This is to ensure that you contribute for a minimum of 20 years. Those above the age of 18 and under the age of 40 are qualified.

Tax Exemptions

The donations you make to the Atal Pension Yojana are tax-deductible. The highest tax exemption permitted under Section 80CCD (1) is 10% of a person’s gross total income. This is limited to Rs. 1,50,000. Consult a tax expert for further information on these exemptions under the Income Tax Act.

Penalty Terms

If you fail to pay for this program, your account will be terminated, and the accrued amount, plus interest, will be refunded to you. If you fail to make a donation on time, you will face the following penalties:

- 1 for monthly payments of up to Rs. 100

- 2 for contributions between Rs. 101 and Rs. 500

- 5 for monthly payments between Rs. 501 and Rs. 1000.

- 10 for monthly payments of Rs. 1001 and more.

Atal Pension Yojana Advantages

- After the contributor reaches the age of 60, a regular monthly pension is sent to them.

- The subscriber can select a pension sum ranging from Rs.1,000 to Rs.5,000, with increments in slabs of Rs.1,000.

- The government would donate 50% of the subscriber’s contribution, or Rs.1,000, to the pensioner’s account for 5 years.

- If the contributor dies while the Scheme is still operational, the monthly pension is given to the spouse and the nominee in a lump sum after the spouse’s death.

- The monthly payment is small and does not impose a financial hardship on the subscriber.

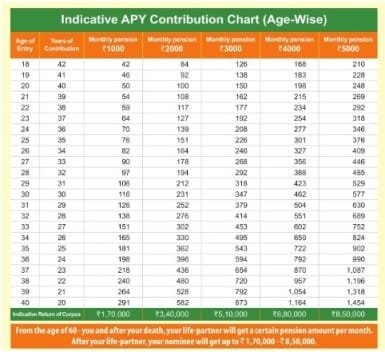

Contribution Chart for the Atal Pension Yojana

If you really want to pay the Atal Pension Yojana on a monthly basis, you must do so according to the chart below. The content is defined amount is determined by your entrance age and the monthly income you seek after retiring.

Procedure for Opening an APY Account

- All nationalized banks provide an APY plan. Anyone can register for the Atal Pension Yojana and set up an account at the bank’s local branch.

- The APY application form may be obtained online by visiting the bank’s official website or the PFRDA’s website. The application form for the Atal Pension Yojana may be downloaded from the website by subscribers.

- The registration form is accessible in Hindi or any other preferred language.

- Complete the Atal pension yojana internet form and send it to the bank.

- In addition to the fully completed form, the subscriber must give a valid cellphone number and a photocopy of their Aadhaar card.

- Upon acceptance of the Atal Pension Yojana application form, the applicant will receive a final text.

Details for completing the APY Form

The following fields must be filled out on the APY Subscriber Registration Form by the subscriber or applicant

Section A: It consists of back details

- Bank Account Number

- Bank Name

- Bank Branch

Section 2: It consisting subscribers’ personal details:

- Name of the Applicant

- Date of Birth

- Email ID

- Marital Status

- Name of the Spouse

- Name of the Beneficiary/Nominee

- Relationship of the subscriber with the nominee

- Age

- Mobile Number

- Aadhaar Card Details for the subscriber,

- nominee, and spouse

Section 3: It consisting subscribers’ Pension Details:

- Pension Amount selected-1000/2000/3000/4000/5000

- Monthly Contribution Amount

Section 4: It consisting Additional Details-If the nominee is a minor:

- Date of Birth

- Name of the Guardian

- Is the minor a beneficiary of other statutory social security schemes?

- Is the minor an income taxpayer?

APY withdrawal procedure

- When you reach the age of 60, you become a senior citizen:

When the subscribers reach the age of 60, they will request the affiliated bank to take the guaranteed minimum monthly pension or a greater monthly pension if investment returns exceed the guaranteed returns incorporated in the APY. When the subscriber dies, the spouse (default nominee) receives the same monthly pension amount. On the death of the subscriber and his or her spouse, the nominee will be entitled to the restoration of the subscriber’s pension wealth accrued up to the age of 60.

- In the event that the subscriber dies after the age of 60 for any reason:

In the event of the subscriber’s death, the same retirement benefits would be useable to the spouse, and if both of them (subscriber and spouse) died, the subscriber’s retirement money collected until the age of 60 would come back to the nominee.

- Exit before the age of 60:

In case a subscriber, who has availed of Government co-contribution under APY, chooses to voluntarily exit APY at a future date, he shall only be refunded the contributions made by him to APY, along with the net actual accrued income earned on his contributions (after deducting the account maintenance charges). The Government co-contribution and the accrued income earned on the co-contribution shall not be returned to such subscribers.

- Death of subscriber before the age of 60:

In case of death of the subscriber before 60 years, the option will be available to the spouse of the subscriber to continue contributing to the APY account of the subscriber, which can be maintained in the spouse’s name for the remaining vesting period till the original subscriber would have attained the age of 60 years. The spouse of the subscriber shall be entitled to receive the same pension amount as the subscriber until the spouse’s death.

Or, the entire accumulated corpus under APY will be returned to the spouse/nominee.

Conclusion

We all know that we need constant support and assistance in this difficult time when people are suffering from the poverty at the age of 60. As a result, the government established the Atal Pension Yojana for the poor and disadvantaged workers of the unorganized sector. The objective of the scheme is to help people save for retirement.

If you require any additional information concerning this Scheme, don’t hesitate to get in touch with us at the following address:

- Contact APY Vinayak Patil, Assistant Manager, at 022-24994596 or vinayakp@nsdl.co.in for customer service.

- Manisha Wayal, the Manager, can be reached at 022-24994522 or via email at manisha.padhye@nsdl.co.in.

1 Response

[…] Click Here for Atal Pension Yojana […]